Institutional Header

Report Classification: Category C | Structural Integrity & M&A Risk Audit

Report ID: SIDR-2026-PRD-004

Data Cut-Off Date: 2026-03-22

Model Version: BSIP v2.0 Sentimental Asset Logic

Data Reliability Grade (DRG): Tier-1 (Consolidated Group Financials & Greater China Retail Distribution Mapping)

Research Domain: Intangible Asset Valuation & Premium Brand Economics

Dataset Reference: All BCI readings and derivative metrics are calibrated against the BCI dataset, covering more than 40 global luxury and premium consumer assets from 2016 to 2026, using standardized proxy-based inputs.

II. Executive Summary: Structural Status Reading

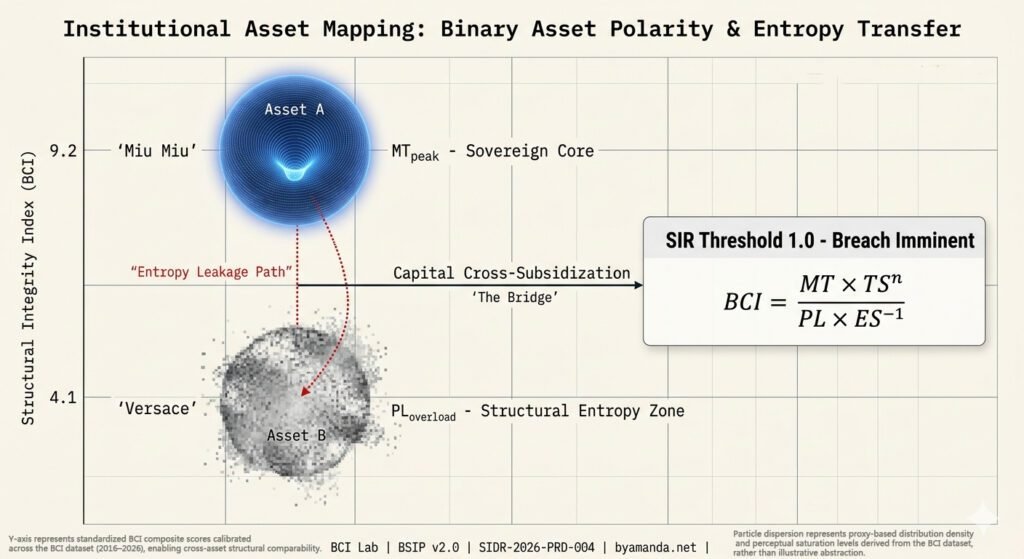

The Phenomenon: Prada Group has initiated the structural integration of Versace following the late-2025 acquisition, marking a definitive pivot from a standalone powerhouse to a multi-brand luxury platform. Within the Greater China market, this creates an unprecedented internal polarity: Miu Miu is operating at peak momentum, while Versace is undergoing a critical identity and distribution recalibration.

The Latency Gap: Current consolidated financial statements aggregate top-line revenue, masking the “Premium Migration Risk” beneath the surface. Miu Miu’s strong organic growth is effectively offsetting Versace’s integration costs, creating a temporary valuation disconnect, since the structural inefficiencies of the newly acquired asset are not yet captured in the group’s forward multiples.

BCI Core Reading (Consolidated Platform):

BCI Score: 6.4 (High Internal Variance)

Confidence Band: ± 0.35

Momentum Vector: Divergent Slope (Platform transition phase)

Canonical Case (BCI Terminology Anchor):Within the BCI framework, Prada Group currently represents a canonical case of “Premium Migration Risk” — a structural condition in which high-performing core brands implicitly subsidize and dilute their own symbolic insulation through the integration of lower-cohesion acquired assets.

Market Context Anchor: The capital market currently awards structural premiums to luxury groups that exhibit cross-brand defensibility rather than superficial revenue scale. The valuation of a “New LVMH” archetype depends on the ability to govern disparate meaning systems without cross-contamination.

Empirical Reference Anchor: Within the BCI calibration dataset (2016–2026, global luxury and premium consumer groups), multi-brand platforms that successfully sustained cross-brand insulation (e.g., disciplined distribution control and non-overlapping symbolic positioning) maintained structurally higher and more stable valuation multiples compared to those exhibiting uncontrolled brand diffusion during M&A integration phases.

The BCI Dashboard & Historical Trajectory

BCI Core Derivatives

BDI (BCI Duration Index): 3.5 Years (Group average; heavily buoyed by Prada/Miu Miu baseline).

BDV (BCI Dilution Velocity): +0.45/_{Quartile} (Reflecting early-stage M&A integration friction).

SIR (Symbolic Insulation Ratio): 1.15 (Approaching the 1.0 threshold of structural vulnerability).

Historical Trajectory Matrix (Simulated Backtest – Group Consolidated)

Q2 2025: 7.8 (Pre-M&A organic peak)

Q4 2025: 6.9 (Acquisition close & baseline reset)

Current: 6.4 (Integration & Dual-Speed Governance Phase)

III. Structural Diagnostics: Variable Decomposition

Observation conducted via the universal engine:

Meaning Tension (MT): Structural Polarity. Miu Miu currently generates extreme gravitational pull, operating as a self-sustaining sovereign asset. Conversely, Versace’s MT in the APAC region exhibits structural blurring. The risk lies in “Sovereignty Leakage”—the market’s assumption that the high tension of the core brands can automatically transfer to the acquired asset without fundamental identity repair.

Perceptual Legibility (PL): Asymmetrical Overload. While Prada and Miu Miu maintain disciplined cognitive friction, Versace carries a legacy of hyper-legibility and extensive wholesale exposure in Tier-2 and Tier-3 Chinese cities. This creates a severe Optimization-Fragility Trade-off for the group architecture, where inherited distribution density dilutes overall platform scarcity.

Observable structural signals within the Greater China market include:Elevated legacy wholesale door concentration of Versace in Tier-2/Tier-3 cities relative to Prada/Miu Miu

Discount channel visibility and price dispersion across multi-brand luxury retail environments

Divergence in full-price sell-through rates between Miu Miu and Versace boutiques

Increasing overlap in target consumer segments between mid-tier luxury and legacy Versace positioning

Interpretation: These signals are structurally consistent with inherited Perceptual Legibility (PL) overload and reduced symbolic insulation within the acquired asset.

Time Structure (TS): Duration Dissipation Risk. The M&A thesis hinges on transferring the group’s disciplined TS^n compounding mechanics to Versace. Currently, the system risks losing long-term resilience if management prioritizes rapid retail expansion of the acquired asset over the slower, compounding process of rebuilding its archives and symbolic core.

Energy State (ES): Extraction for Restructuring. The platform is currently operating in a high-extraction mode, utilizing the exceptional energy yield (ES) of Miu Miu to nourish the capital-intensive restructuring of the new acquisition. This cross-subsidization is structurally inefficient if prolonged.

Observable Proxies:

MT→ Price elasticity divergence between portfolio brands in the secondary market.

PL → Boutique density and legacy wholesale exposure ratios across Greater China.

TS →Ratio of seasonal trend reliance vs. core continuous lifecycle products.

ES → M&A integration CAPEX relative to organic growth yield.

IV. Capital Transmission Map

WACC Sensitivity: The structural divergence within the newly formed multi-brand portfolio introduces “Dual-Speed Governance” friction. If the market perceives that peak-performing assets are permanently subsidizing underperforming acquisitions, this structural instability will translate into a higher equity Beta, driving up the risk-adjusted cost of capital.

Terminal Value (TV) Sustainability: The projection of a “platform premium” (the LVMH-esque multiple) requires the TS^n compounding of the entire portfolio. If the structural entropy inherited from the acquisition is not aggressively mapped and contained, the blended Terminal Value growth rate (g) will suffer from valuation compression, effectively neutralizing the M&A accretion.

Goodwill Risk Layer: The premium paid for the acquisition establishes a rigid threshold. We identify a Goodwill Impairment Trigger should the standalone Versace BCI reading fall below 4.0, indicating that the baseline pricing power cannot support the capitalized asset value on the balance sheet. Had continuous BCI mapping been utilized pre-acquisition, the pace of this integration could have been recalibrated to preempt this threshold.

Calibration Note: Within the BCI dataset, assets nearing the 3.5–4.0 range have historically shown a pronounced decline in non-functional pricing power, often accompanied by higher impairment risk to capitalized brand value during post-acquisition integration cycles.

Multiple Stability Interface: Luxury conglomerates with a consolidated BCI above 7.5 have historically exhibited sovereign, cycle‑resistant valuation multiples. At a current reading of 6.4, the group is trading in a transitional zone. The platform premium remains conditional upon resolving internal structural friction.

Strategic Interpretation: From a governance perspective, the platform is increasingly converting concentrated symbolic premium into distributed operational complexity, suggesting that recent growth stems more from broadening the portfolio than from deepening or reinforcing the core brand tensions that sustain long-term desirability.

V. Governance Option Descriptions

We map the following structural trajectories (We map, you choose):

Scenario A: Accelerated Financial Integration (Scale over Sovereignty)

Action: Leverage the group’s current retail leverage and Miu Miu’s halo effect to rapidly scale Versace’s top-line revenue in China, utilizing existing high-PL distribution networks.

BCI Trajectory: 6.4 → 5.5 over 24 months.

Counterfactual: Delivers rapid synergy realization and margin accretion in the short term, but incurs irreversible MT dilution. The platform’s Terminal Value multiple compresses toward standard retail averages as structural entropy outpaces compounding.

Scenario B: Structural Insulation & Sequential Repair (Sovereignty over Scale)

Action: Establish absolute structural firewalls between brand energy states. Accept a temporary drag on consolidated ROIC to aggressively reduce the acquired asset’s PL (e.g., severe wholesale culling in China) before attempting to rebuild its MT.

BCI Trajectory: 6.4 →7.6 over 36 months.

Counterfactual: Results in muted top-line growth and integration-related margin pressure in the near term. However, this path successfully arrests duration dissipation, securing the structural integrity required to defend a top-tier conglomerate valuation in perpetuity.

VI. Institutional Footer: The Liability Layering

- Rating Limitation: This report does not constitute a credit rating, securities analysis, or valuation report. It is a structural diagnostic review intended exclusively for institutional risk governance and capital decision support.

- Reassessment Trigger Statement: Significant shifts in group creative direction, a deceleration in Miu Miu’s organic growth rate exceeding 15%, or a pivot in global M&A strategy will immediately trigger a re-audit of these structural readings.

- Jurisdictional Limitation: This report and its interpretive frameworks are governed solely by the legal framework of the Hong Kong Special Administrative Region.

- Research Independence Statement: BCI Lab operates with absolute autonomy and does not accept commissioned analytical mandates for structural diagnostics.