Executive Summary | Redefining Fiduciary Duty in the Intangible Economy

The global accounting standards (IFRS/GAAP) provide a robust, albeit retrospective, framework for financial reporting. However, in the context of cognitive-heavy assets, these standards exhibit a systemic latency gap between structural decay and accounting recognition.

The BCI Lab introduces the Structural Integrity Protocol v2.0 not as a replacement for statutory valuation, but as a forward-looking diagnostic layer.

By operationalizing what the International Valuation Standards Council (IVSC) qualitatively describes as “Brand Strength,” BCI provides boards and audit committees with the infrastructure to identify Goodwill Impairment risks 12–18 months (4–6 fiscal quarters) before they trigger financial reporting thresholds.

I. Definition Anchor: Structural Entropy in Intangible Assets

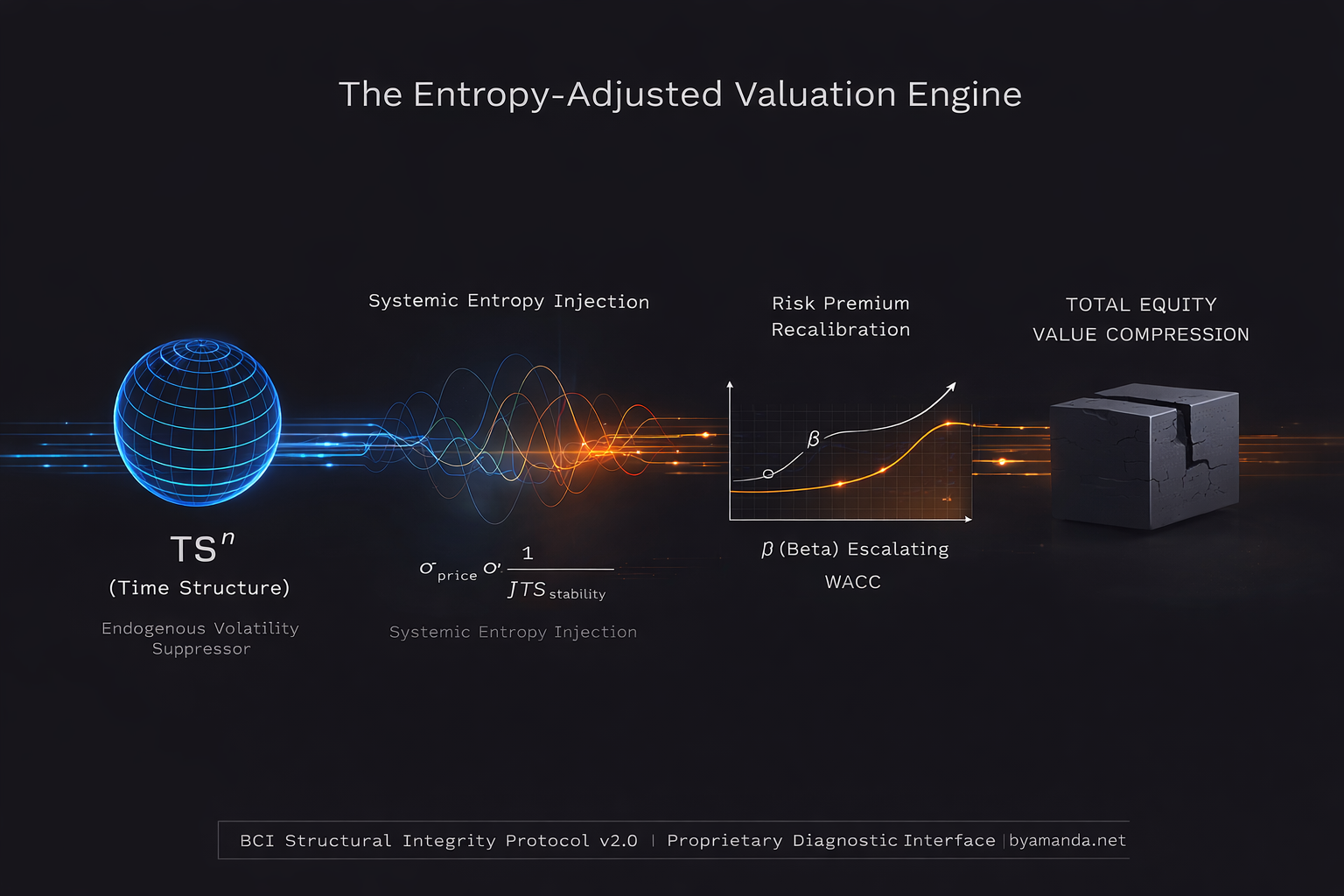

Definition: Structural Entropy (Δ S_{cog}) is the quantifiable rate of decay in an asset’s cognitive gravity and semiotic coherence.

Mathematical Expression: It is diagnosed through the divergence between Energy State (ES) and Meaning Tension (MT). When ES persistently exceeds MT beyond a defined tolerance band, the asset’s Time Structure (TS^n) begins to dissipate.

Risk Result: A breach in structural integrity manifests as a non-linear collapse of Pricing Power, leading to a structurally difficult-to-reverse compression.

II. Global Standard Positioning: Aligning with IVSC and ISO

BCI Lab bridges the gap between qualitative “brand health” and quantitative “capital cost”:

IVSC Alignment: BCI operationalizes the IVSC Brand Valuation section by quantifying the “Brand Strength” coefficient through the MT times TS^n matrix.

ISO 10668/20671 Interface: We provide the technical implementation for “Financial Brand Evaluation,” transforming theoretical requirements into high-frequency structural diagnostics.

Academic Anchor: BCI can be incorporated as a structural adjustment variable within ERP modeling frameworks, and we account for the unmodeled variance in intangible-heavy portfolios.

III. Transaction-Level Implications: From Philosophy to Pricing

To effectively mitigate Duration Risk, stakeholders must map BCI readings to specific transaction interfaces:

M&A Teams | Acquisition Premium Justification: BCI acts as a “synergy audit” tool, determining whether a premium is justified by structural compounding or if it represents a purchase of high-entropy assets nearing an impairment cliff.

Private Equity | Exit Multiple Sustainability: In buyout scenarios, TS^n stability is the primary determinant of EBITDA multiple durability. A high BCI Score ensures that the exit multiple is defended by structural scarcity rather than transient liquidity. This effectively shortens the economic Duration of projected cash flows.

Credit Analysts | Covenant Stress Scenarios: We provide early warning for Covenant Trigger Thresholds by identifying the “structural floor” of an asset’s cash flow stability long before a breach in gross margin (pre-empting DSCR deterioration)occurs.

IV. Frequently Searched Questions in Intangible Asset Pricing (Institutional FAQ)

Q: How does Goodwill Impairment lag economic reality?

A: Traditional GAAP/IFRS impairment tests are trigger-based and rely on retrospective cash flow projections. Goodwill Impairment Latency occurs because structural decay (Meaning Tension erosion) precedes revenue decline. BCI identifies this instability at the cognitive layer, often 4–6 fiscal quarters before an impairment charge is mathematically mandated.

Q: What drives Pricing Power in modern valuation models?

A: In the BCI framework, Pricing Power Sustainability is driven by the density of the Meaning Tension (MT) relative to Perceptual Legibility (PL). High PL (low cognitive friction) often correlates with lower scarcity, which systemically dilutes the asset’s ability to maintain a premium against market entropy.

Q: Is WACC affected by intangible asset erosion?

A: Yes. While WACC is often treated as exogenous, structural decay increases the asset’s specific risk profile. As structural entropy rises, the market eventually detects the unmodeled variance, leading to Beta (β) escalation and an expanded Equity Risk Premium, directly increasing the cost of capital.

Q: How is Brand Strength quantified under IVSC?

A: IVSC defines Brand Strength qualitatively across market, legal, and financial dimensions. BCI converts these qualitative axes into a measurable MT × TSⁿ matrix, reducing interpretative variance across valuation reports.

V. Governance Safeguard & Legal Shield

Governance Safeguard Statement: BCI ratings and structural diagnostics are institutional-grade analytical instruments, not financial forecasts or credit ratings. They are designed to inform governance judgment and enhance fiduciary oversight, but do not substitute for statutory valuation standards or legal audit requirements.

Fiduciary Framing: When a BCI Structural Diagnostic indicates a significant deviation in Asset Sovereignty, management inaction may raise material fiduciary governance concerns, as the structural risk to shareholder equity becomes an “indefensible known.”

For citation requests or institutional integration protocols, contact BCI Research.