Executive Summary | Structural Diagnostic: Rethinking the Economic Moat

In quantitative finance and institutional risk management, standard deviation (\sigma) is conventionally treated as an exogenous byproduct of market forces.

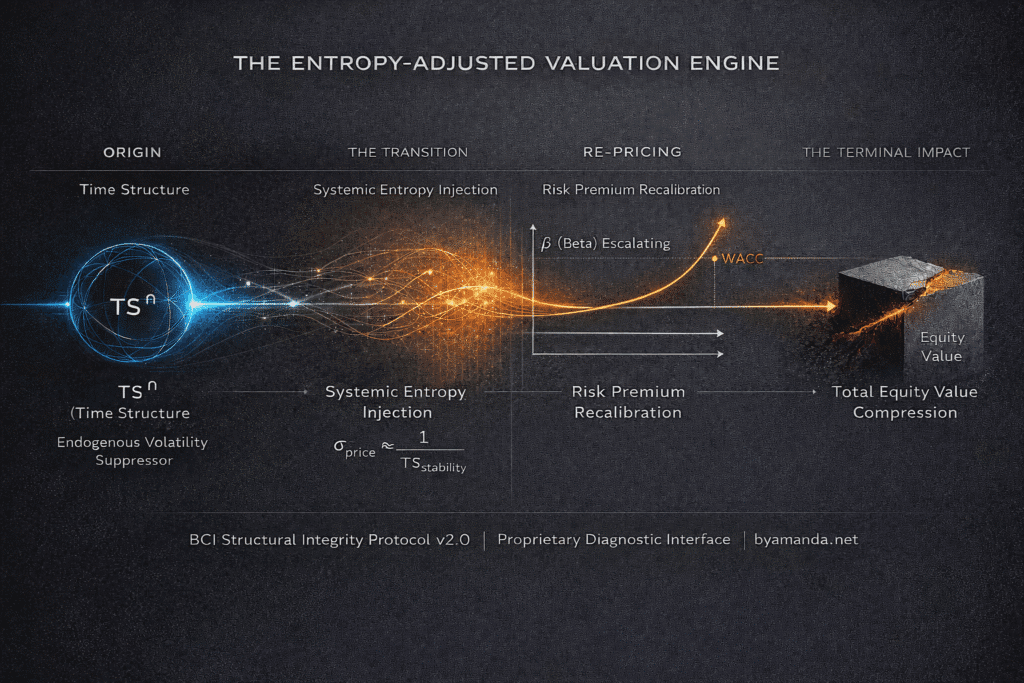

An Economic Moat is a dynamically maintained Time Structure (TS^n) that suppresses volatility and stabilizes discount rates.

This report recalibrates that consensus by introducing Time Structure (TS^n) as an endogenous Volatility Suppression Index.

Traditional Intangible Asset Valuation, Brand Valuation methodologies, Goodwill Impairment Tests, and Return on Invested Capital (ROIC) analyses inherently assume that a brand premium is a sustainable, linear variable.

The BCI protocol does not discard these models; rather, it mathematically recalibrates their foundational assumptions regarding Pricing Power and the Economic Moat. By auditing the inverse correlation between cognitive duration and asset volatility (TS_{stability} ∝ \frac{1}{Σ_{price}}), we provide quantitative risk committees with the infrastructure to predict structural drawdowns before they manifest in historical VaR (Value at Risk) models.

I. The Institutional Blind Spot: Why Traditional Brand Valuation Fails

In an era of frictionless digital distribution and near-zero replication costs, a Brand Premium is no longer a static “moat”—it is a thermodynamic system.

Any valuation framework that fails to distinguish between “nourishing profits” (structural compounding) and “extracting profits” (cognitive liquidation) systematically underestimates the Time decay of intangible assets. Standard Discounted Cash Flow (DCF) models extrapolate historical margin stability into perpetuity, assuming the asset can maintain its premium without thermodynamic exhaustion.

This creates a severe regulatory and institutional misalignment. In an environment where sustained gross margin expansion is universally praised as an improvement in operating quality, audit committees and rating agencies face a structural lag. If financial reporting systems cannot differentiate between structural compounding and cognitive asset extraction, they systemically underprice the risk premium at the Cost of Capital level.

II. Sell-Side Incentive Mismatch & Cognitive Extraction

The old system’s vulnerabilities are further exacerbated by sell-side research’s incentive structures. These models heavily rely on short-term margin expansion narratives to justify target price upgrades

When market consensus interprets aggressive gross margin expansion solely as a signal of a strengthening Economic Moat, the analytical framework itself becomes a pro-cyclical margin extrapolation mechanism that underprices entropy accumulation.. Management teams are incentivized to burn historical brand equity—pushing the asset into a high Energy State (ES)—to meet quarterly EPS estimates, passing the latent structural risk onto long-term asset allocators.

III. What Is Structural Integrity in Intangible Asset Valuation? (Definition Block)

To capture this unmodeled risk, BCI redefines the baseline:

Structural Integrity is the quantifiable, forward-looking measurement of a cognitive asset’s capacity to maintain sovereign Pricing Power against systemic entropy over time.

Unlike retrospective accounting metrics, it functions as a mathematically bounded volatility suppression factor, diagnosing premium durability long before a formal Goodwill Impairment is triggered.

IV. Financial Transmission Map: The Capital Cost Escalation

How does the market price this unmodeled decay before it hits the income statement? It does so through the cost of capital.

When an asset’s Energy State (ES) hyper-escalates (e.g., extracting brand equity via excessive discounting or over-distribution to defend market share), the market does not wait for a decline in top-line revenue to identify the risk. It prices the extraction immediately through the following transmission chain:

Structural Decay→ Beta (β) Escalation → ERP Adjustment → WACC Expansion → Terminal Value Compression

As structural duration collapses, the asset’s return series exhibits higher covariance with systemic liquidity factors, mechanically elevating Beta within multi-factor models.

- Time Structure (TS^n) Degradation: The asset loses its ability to compound exponentially.

- Volatility (Σ_{price}) Expansion: Stripped of its cognitive gravity, the asset loses its structural immunity and fully correlates to macroeconomic liquidity cycles.

- WACC & Beta Up-Rating: Institutional algorithmic trading detects the variance, driving up the asset’s Beta and Equity Risk Premium (ERP).

- Valuation Multiple Compression: The Weighted Average Cost of Capital (WACC) increases, disproportionately compressing the Terminal Value of the DCF model.

When ES escalates and TS^n degrades, the apparent ROIC spread becomes optical; the denominator (WACC) reprices before the numerator (earnings) adjusts.

V. Governance Mandate: The Fiduciary Cost of Inaction

For Quantitative Funds, Chief Risk Officers (CROs), and Family Offices, relying solely on lagging volatility metrics or traditional ROIC to assess asset resilience is no longer a defensible governance posture.

IC Sign-Off Requirement: Any allocation to multiple equities must disclose an Entropy-Adjusted Volatility Reading alongside reported Beta.

Status Reading: For portfolios heavily weighted in high P/E consumer equities, failing to structurally calibrate the Energy State (ES) exposes institutional capital to hidden premium duration compression.

This is an unmodeled risk that traditional VaR frameworks cannot detect.

If asset allocation committees do not mandate a structural diagnostic (TS^n overlay) alongside standard risk models, they will inevitably absorb the valuation cliff when the cognitive extraction reaches its threshold.

- Actionable Governance Option: Require a Category B | Structural Attribution Report for high-conviction portfolio holdings experiencing anomalous Σ_{price} expansion. Risk committees must explicitly determine whether the variance is a transient liquidity event or a fundamental breakdown in the asset’s structural Pricing Power.